Insurance sales doesn’t stall because agents don’t care. It stalls because too many moving parts drag on each other. Leads trickle in from web forms, referral links, quote engines, call centers, and partner portals. Compliance adds rules that vary by product and region. Carriers change underwriting guidelines. Marketing wants attribution, sales wants speed, service wants accurate handoffs, and nobody wants another swivel-chair workflow that burns hours and morale.

Agent Autopilot exists to stitch these parts into a rhythm. Not the chaotic kind with three tools barking at the same time, but a measured cadence that recognizes context, chooses the right channel, and nudges the next best action at the right moment. Think of it as a policy CRM aligned with secure data handling principles and built for omnichannel outreach that doesn’t spam. It listens, scores, prioritizes, and routes, then measures every step so you can prove what’s working and retire what’s not.

What “autopilot” means in insurance outreach

Autopilot doesn’t mean set-and-forget. It means your system anticipates a likely outcome, proposes the move, and carries it out with governance controls. A prospect who requested a homeowners quote yesterday gets a text to confirm property details, not a generic newsletter. A lapsed auto policyholder receives a renewal rescue sequence with the right disclosures, sent within allowed hours in their state. A commercial prospect browsing cyber riders on your site triggers an outbound call only if the account’s risk score and potential lifetime customer value justify agent time.

Under the hood, this requires three disciplines working in concert: data hygiene, decisioning, and delivery. Data hygiene cleans and verifies contact and policy records. Decisioning evaluates intent from signals and history. Delivery executes the engagement across email, SMS, voice, chat, and social messaging, then writes back performance. When teams try to do these by hand or across disjointed tools, you see dropped deals and fuzzy attribution. When they run through one workflow CRM for measurable agent efficiency, you feel the slack come out of the system.

Real-time lead scoring that earnestly prioritizes

Any insurance CRM with real-time lead scoring has to account for more than form fills. The signal is richer: quoting behavior, underwriting flags, inbound phone sentiment, referral sources, eligibility pre-checks, credit bands where permitted, and household composition. Real-time, in practice, means a score refreshes the moment a relevant event occurs. If a lead completes a quote, the score changes before an agent even opens the record. If a competitor sends a cancellation notice through a data feed, the model bumps urgency.

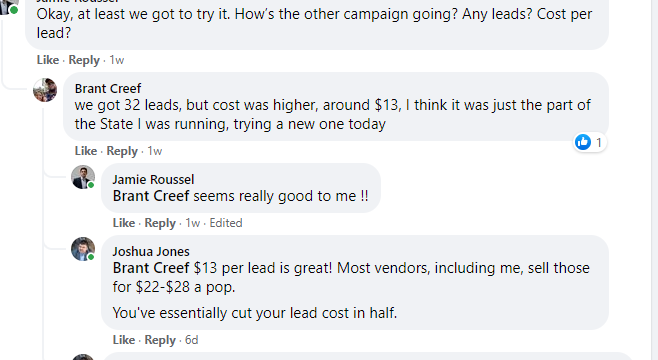

I’ve seen teams chase the wrong thing because a static score looked great on paper. One carrier’s top decile based on demographic fit underperformed by 30 percent compared to a mid-tier segment that clicked on coverage endorsements twice within a week. Behavioral signals trump assumptions more often than not. When you adopt an AI-powered CRM for high-efficiency policy sales, insist on models that can ingest both structured and unstructured signals, then prove their lift in A/B tests rather than faith.

Practical tip: make the score interpretable. An agent who sees “88” without context doesn’t change behavior. Show the three drivers that matter: recent quote completion, previous claim with competitor, and price sensitivity inferred from multi-quote comparisons. That’s how you turn scoring into action, not trivia.

Orchestrating omnichannel without annoying people

Omnichannel outreach works when each nudge respects the person’s preferences and the regulatory environment. Some prospects want email summaries they can read after dinner. Others want a quick text and a link to e-sign. Enterprise buyers in benefits expect scheduled calls and clean recap notes. Agent Autopilot builds contact plans that honor opt-ins and quiet hours, enforce disclosures, and record consent updates in the same system that manages campaigns.

The difference shows up in deliverability and response times. One agency I worked with cut unsubscribes by 40 percent simply by stopping duplicate outreach on the same day from marketing and sales. We connected the marketing automation to the workflow CRM for compliance-based agent outreach, so a prospect who clicked a quote CTA automatically paused nurture emails and jumped to an agent-led sequence. Messages stopped stepping on each other. Response rates went up without increasing volume.

Outbound automation matters, but inbound often wins the deal. An AI CRM with outbound and inbound automation tools should turn a missed call into a recovery path: instant voicemail transcription, a text asking for a better time, a link to a self-serve quote revision, and a task for the agent with the context attached. Most systems do some version of this. The difference is how quickly all of it updates the record and whether an agent can see, at a glance, what happened and what’s next.

Multi-agent collaboration that doesn’t turn into a relay race

Insurance rarely sells and services through a single person. You may have producers, inside sales, customer success, and service reps touching the same compliant ACA lead specialists agentautopilot.com household or account. Without a workflow CRM for multi-agent collaboration, files drift into email chains, and someone inevitably calls a client who already answered that question. The fix isn’t more chat; it’s smarter handoffs and shared visibility.

I like “playbooks” that define who owns a stage and by what SLA. For example, when a personal lines homeowner request includes a secondary short-term rental, the system routes to a specialist within two hours, then loops the original agent back in for the bind-and-welcome call. Notes and documents live on the policy record, not in someone’s inbox. When a cross-sell opportunity surfaces for umbrella coverage, the policy CRM for cross-department sales optimization alerts the right teammate with the underwriting checklist pre-filled from existing data.

Coordination should be measurable, not just polite. Track assist rates and time-to-handoff. In a healthy motion, assist rates rise as specialists add value while cycle times fall. If assists spike but deals slow, you’ve added friction, not expertise. Treat those signals as product metrics for your sales process.

Renewal discipline separates healthy books from leaky ones

Everyone says renewals matter. The questions are when do you start, how do you personalize, and how do you avoid fatigue. A policy CRM trusted for accurate renewal processing does three things well: aligns carrier rules with your outreach timetable, highlights risk of churn based on rate changes and life events, and automates payment and documentation steps with minimal back-and-forth.

Start the conversation based on anticipated impact. If a customer faces a 2 to 4 percent increase with no claims, your message is a confidence builder with a quick confirmation path. If a 12 percent jump is likely, you reach out earlier, acknowledge the change, and offer options. I’ve seen renewal saves improve by 10 to 15 percent when agents approach pricing changes with context rather than generic pleas to stay.

The mechanics matter. Pre-fill renewal forms, update contact preferences, and route follow-ups based on response channel. A trusted CRM for measurable sales retention can surface an exception queue: policies with exposure changes, missing inspections, or lapsed payment methods. Agents don’t sift. They act.

Predictive account management that respects underwriting reality

There’s a fine line between helpful prediction and wishful thinking. Forecasts should guide prioritization, not override underwriting. An AI-powered CRM with predictive account management earns its keep when it flags: households approaching life events like a teen driver, commercial accounts entering a renewal market with appetite shifts, or clients who recently interacted with pricing pages suggesting sensitivity.

Accuracy isn’t a single number. I prefer calibrated probability ranges. If the system says there’s a 60 to 70 percent chance of bundling success for a specific household, I want to know which variables drove that: claim-free period, home security discount, prior inquiries about auto, and recent credit tier improvement where allowed. Agents can push back with field knowledge. If your CRM can’t capture that field override with a reason code, you’re losing training data that would improve the model.

Compliance as a design constraint, not an afterthought

Every insurance outreach tool claims compliance. The question is whether the workflow CRM for compliance-based agent outreach builds compliance into the journey. Consent capture should be granular: separate toggles for SMS, email, and voice. Disclosure language must update centrally and populate consistently across templates. Quiet hours and regional rules need to be enforced at send time, not depend on agents remembering a binder note.

Audit trails matter more than bragging rights. Every touch should have a timestamp, the content that was sent, the channel, and the consent state at that moment. If a regulator asks, you produce the record without scramble. This level of rigor pairs with policy CRM aligned with secure data handling: encryption, role-based access, data retention policies, and clear boundaries between marketing and underwriting data where necessary.

Measuring what matters so you can prove return

What you measure shapes behavior. Vanity metrics like total emails sent or raw pipeline volume can quietly punish the right actions. Focus on conversion-weighted activity and cost per written premium by channel and segment. An insurance CRM trusted for data-driven campaign insights should show agent-level, team-level, and segment-level outcomes without requiring exports and spreadsheets to make sense of it.

Don’t stop at new business. Track lifetime customer value projections and actuals. With an insurance CRM with lifetime customer value tracking, you can justify service touches that don’t show immediate revenue but protect the book. A periodic coverage review, for example, might not sell today, yet it reduces churn risk by reminding clients they’re cared for and fully covered.

One practical way to make metrics stick: publish a weekly “route-to-value” digest. It shows which sequences produced the most Insurance Leads bound premium, which assisted handoffs closed faster, and where compliance holds prevented a mistake. Keep it short, keep it honest, and let teams suggest experiments. Over time, you’ll see a culture of measured improvement, not shotgun tactics.

Building a sales motion that accommodates both speed and care

Speed wins quotes. Care wins households. When the tools are flexible enough, you don’t have to choose. A trusted CRM for conversion-focused sales teams should let you define contact strategies by product complexity. Simple monoline auto can ride a fast lane: instant quote, two-touch close, e-sign. More complex commercial accounts benefit from discovery calls and documented risk assessments. The system adapts, not forces one path.

I’ve seen producers double their close rate on small business packages by using a short intake form that prequalifies appetite, then sending a guided calendar link that blocks time with an underwriter on the call. That workflow felt high-touch to the client and saved back-and-forth emails. Your CRM must make this easy: templates, booking integrations, and record updates in one motion.

Getting the data model right on day one

Bad data ruins the best automation. Before you dream up fancy sequences, get your entities straight: person, household, policy, quote, claim, activity, and consent artifacts. Think through one-to-many relationships: multiple policies per household, multiple drivers per vehicle, multiple locations per commercial account. If you mash these into a single flat record, you’ll be rewriting flows every quarter.

Map source systems carefully. Carriers, quote engines, phone systems, and marketing platforms each speak a slightly different dialect. Set up transformation rules once, test them with real records, and keep a change log. The first 90 days determine whether you trust the system. If agents spot missing drivers or outdated addresses, adoption suffers. Assign a data steward early, not after issues pile up.

Omnichannel playbook examples you can adapt

Consider three common motions that benefit from orchestration:

- Warm lead-to-bind in personal lines: Web lead enters with home address and desired coverage. Real-time lead scoring bumps urgency due to prior quote history. System triggers a text confirming details and offers a callback window. If no response in one hour, an email with a custom premium range goes out. Agent sees a single “next best action” tile: call with inspection checklist attached. Commercial renewal at risk: Rate lift over 10 percent and two unanswered service tickets. CRM creates a save plan: schedule a risk review call, send a coverage summary, and open a referral to a market with better appetite. Compliance gates ensure only approved language is used. Progress is visible to producer and service team. Cross-sell to existing auto book: The insurance CRM built for EEAT marketing workflows identifies households that engaged with home safety content, have solid credit where applicable, and no claims in three years. An educational email leads to a calculator, followed by a one-click request for a bundled quote. Agents receive a ranked list and a concise talk track tailored to the segment.

Each playbook blends outbound and inbound paths and draws on a common data spine. The specifics vary by line and region, but the structure holds: clear trigger, channel sequence that respects consent, a crisp agent task, and measurable outcomes.

Reducing agent toil without losing their voice

Agents bring craft that software can’t replicate. The goal is to free their time for conversations where judgment matters. Start by identifying repetitive tasks that don’t require creativity: logging calls, updating contact info, checking policy numbers across systems, sending the same three follow-up emails. Your workflow CRM for measurable agent efficiency should handle these with templates and smart defaults, while giving agents room to edit and add personality.

Voice matters. A canned email can sound cold if it bulldozes a sensitive situation. Good systems offer content blocks that agents can assemble. Think reusable paragraphs for rate explanations, deductible education, or inspection prep, which agents personalize with a sentence or two. Over time, your best-performing phrasing becomes a shared library, not a script that turns everyone into the same voice.

What to expect during rollout

The first month sets the tone. You don’t need a massive bang. Pick one line of business and one or two sequences that tie to revenue: new quote follow-up or renewal rescue, for example. Integrate your quote engine and telephony, then run a two-week pilot with five to ten agents. Measure response times, conversion rates, and agent satisfaction. Ask the hard questions: did the system add clicks, did it surface the right next action, did it get in the way?

Expect some friction where old habits meet new workflows. One agency I worked with saw agents bypass the CRM dialer because they preferred their personal cell process. Rather than scolding, we configured caller ID to show the local agency number and made voicemail drops optional. Adoption rose because the system respected how agents actually work.

Security reviews and compliance approvals take time. Bring those teams in early. If your policy CRM aligned with secure data handling can show encryption standards, access logs, and consent architecture upfront, you avoid late-stage rework.

From insight to improvement: a cadence that compounds

Implementation is step one. The compounding value comes from a rhythm of review and test. Every month, examine three dashboards: lead-to-bind conversion by source and segment, renewal retention by bucketed rate change, and assist/handoff effectiveness by team. Pick one hypothesis. Maybe your SMS step fires too early in the journey. Maybe your cross-sell talk track is too long. Change one variable, measure for two weeks, and keep score.

Over six months, the shape of your book changes. You write more policies without burning out your team, not because volume increased, but because waste decreased. Multi-agent collaboration runs smoother, and leaders can link activities to outcomes. A policy CRM trusted for accurate renewal processing and an insurance CRM trusted for data-driven campaign insights earn those labels by proving results you can point to, not logos on a slide.

A quick checklist to evaluate readiness

- Data foundations: Are household, policy, quote, and consent objects accurate and consistently populated? Consent discipline: Can you prove channel-specific opt-ins with timestamps and content versions? Agent workflow fit: Do agents complete their day inside the CRM without hopping tools for basic tasks? Measurement clarity: Can you attribute bound premium to sequences and channels without manual spreadsheets? Governance comfort: Are compliance, security, and legal teams clear on controls and audit trails?

If three or more of these are shaky, invest there before dialing up automation. Autopilot amplifies what’s underneath. It can’t fix a broken airframe.

Where the market is heading and how to stay sane

The industry is marching toward more data sources, tighter regional rules, and buyer expectations shaped by consumer apps. The temptation will be to chase the newest feature. Resist. The winners will be those who master the basics, then add intelligence where it clearly moves the needle: an insurance CRM with real-time lead scoring that surfaces the right call at the right time; omnichannel orchestration that respects consent and context; and predictive nudges that help, not hype.

When done well, an AI-powered CRM for high-efficiency policy sales doesn’t feel like software at all. It feels like a team rhythm that honors each customer’s path. Agents spend their time where it matters, managers see cause and effect, compliance sleeps better, and customers get clear, timely help instead of noise. That’s the kind of autopilot you keep on not because you have to, but because the ride gets smoother for everyone.